Estate planning sounds like something for your parents. Or for people with beach houses and stock portfolios and gray hair. Not for a 34-year-old physician who just started making real money two years ago.

But consider what your life actually looks like right now: you earn ~$340,000 a year. You have a spouse and a toddler who depend on that income entirely. You have a mortgage. You have $200,000 in student loans. You might have $50,000 in a 401(k) and a term life insurance policy you bought last year. And you practice medicine — which means you carry professional liability exposure that most people in other careers don't.

If you died tomorrow without an estate plan, here is what would happen to your family in California: a court would decide who raises your child. A judge — a stranger — would appoint someone to manage your finances. Your spouse would wait 12 to 18 months to access your assets, while paying $46,000 or more in statutory probate fees on a $1 million estate. And all of it would be a matter of public record.

If you became incapacitated — a traumatic brain injury, a stroke, a severe illness — your spouse would need to petition a court for conservatorship just to make financial decisions on your behalf. That process is expensive, invasive, and can take months.

A will alone doesn't prevent any of this. Here's what does.

Why a Will Isn't Enough in California

A will does one thing well: it tells the court who should get your stuff and who should raise your kids. But a will doesn't avoid probate — it goes through probate. It's an instruction manual for the court, not a bypass around it.

California's probate fee structure is statutory — set by Probate Code Section 10810 — and it's one of the most expensive in the country. Both the attorney and the personal representative (executor) each receive fees based on the gross value of the estate: 4% of the first $100,000, 3% of the next $100,000, 2% of the next $800,000, and 1% of the next $9 million. Those fees are calculated on gross value, not net equity. Your home's full appraised value counts, regardless of how much you owe on it.

During probate, your family's ability to access bank accounts, sell property, or make financial decisions is severely constrained. There's a mandatory four-month creditor claim period that cannot be shortened. Court backlogs in Los Angeles County frequently push the total timeline beyond 18 months. And the entire proceeding is public — anyone can look up the value of your estate, who your beneficiaries are, and what they received.

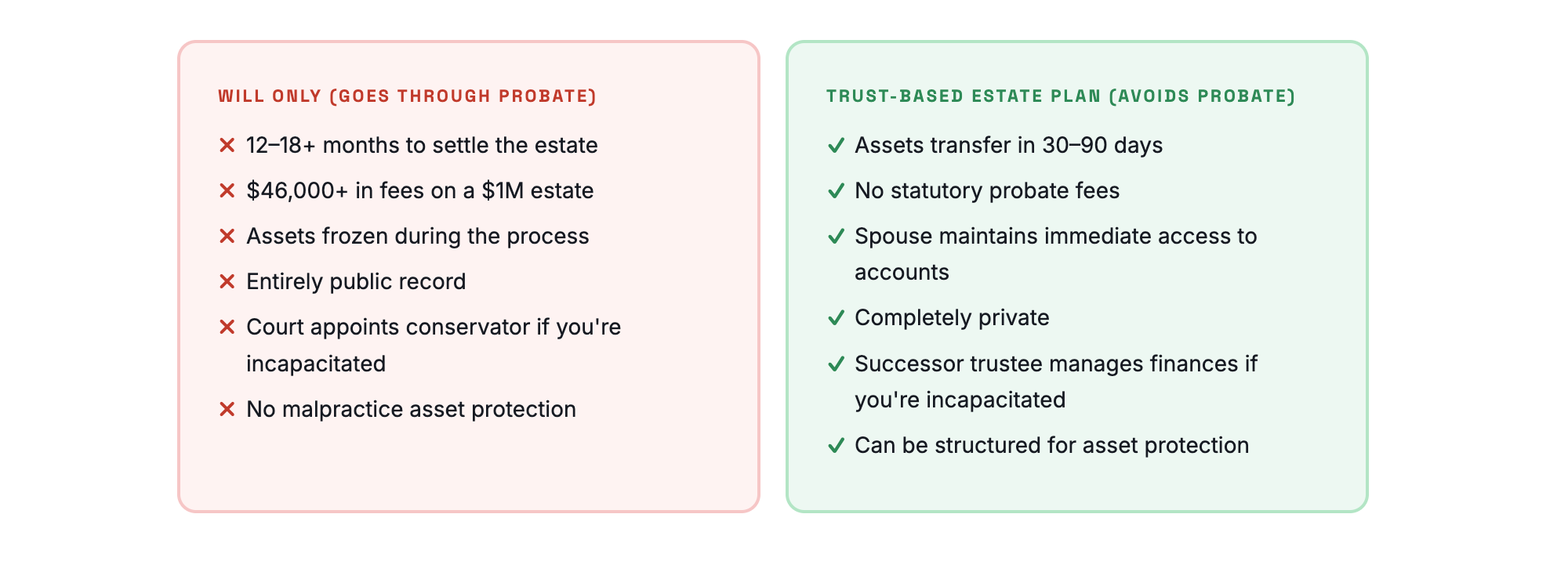

- 12–18+ months to settle the estate

- $46,000+ in fees on a $1M estate

- Assets frozen during the process

- Entirely public record

- Court appoints conservator if you're incapacitated

- No malpractice asset protection

- Assets transfer in 30–90 days

- No statutory probate fees

- Spouse maintains immediate access to accounts

- Completely private

- Successor trustee manages finances if you're incapacitated

- Can be structured for asset protection

What a Complete Estate Plan Looks Like at 34

A trust-based estate plan for a young physician household isn't a thick binder of legal documents that gathers dust on a shelf. It's a working set of instructions that handles three scenarios: you die, you become incapacitated, or you're fine and your assets continue growing under a structure that protects them.

| Document | What It Does | Why You Need It Now |

|---|---|---|

| Revocable Living Trust | Holds your assets outside of probate. Names a successor trustee who can manage everything immediately if you die or become incapacitated. You retain full control while alive. | Avoids the $46K+ probate process, keeps everything private, and gives your spouse immediate access to funds. |

| Pour-Over Will | Catches any assets that weren't transferred into the trust during your lifetime and directs them into the trust at death. | Acts as a safety net. Assets caught by the pour-over will still go through probate, which is why properly funding the trust is essential. |

| Financial Power of Attorney | Designates someone to make financial decisions if you're unable to (without going to court for conservatorship). | Without it, your spouse would need a court order to access your accounts or manage your finances after a serious accident or illness. |

| Advance Healthcare Directive | Designates someone to make medical decisions for you and documents your wishes regarding end-of-life care. | As a physician, you understand the importance of clear medical directives. Your family shouldn't have to guess. |

| Guardian Nomination | Names who will raise your minor children if both parents die. | Without a nomination, a court decides. This is the most emotionally important document in the entire plan. |

| Beneficiary Designations | Controls who receives your 401(k), IRA, life insurance, and any TOD/POD accounts — these pass outside of both probate and your trust. | Outdated beneficiaries (an ex-spouse, a parent from residency) can override your will and your trust. Review these every year. |

The typical cost for a trust-based estate plan from a qualified estate planning attorney is $2,500 to $5,000. On an estate that would otherwise pay $46,000+ in probate fees, the plan pays for itself roughly 10x over.

The Physician-Specific Layer

Everything above applies to any high-earning California household with kids and a mortgage. But physicians have an additional set of considerations that make estate planning both more urgent and more complex.

Malpractice Liability and Asset Protection

Physicians face professional liability exposure that most other professionals don't. While malpractice insurance covers claims up to your policy limits, a judgment that exceeds those limits reaches into your personal assets. In California — a community property state — that potentially exposes assets held jointly with your spouse.

Certain trust structures, asset titling strategies, and insurance configurations can create layers of protection. This isn't about hiding assets — it's about structuring ownership so that a single adverse event doesn't destroy a family's financial future. We covered the full framework in our guides on protecting physician assets from malpractice lawsuits and asset protection for high-net-worth individuals in California.

Disability Is More Likely Than Death

At age 34, you are statistically more likely to become disabled than to die. The Social Security Administration estimates that 1 in 4 of today's 20-year-olds will experience a disability before reaching retirement age. A durable financial power of attorney and a properly structured trust with an incapacity provision ensure that your spouse can manage finances, pay bills, make investment decisions, and access accounts without petitioning a court — a process that can take months and cost thousands in legal fees.

Without these documents, your spouse could be locked out of your own bank accounts while you're in the ICU. That's not a theoretical risk for physicians — it's a scenario that plays out more often than most people realize.

Community Property and Physician Income

California is one of nine community property states. Income earned during the marriage belongs equally to both spouses, regardless of who earned it. This has significant estate planning implications: if you die, only your half of community property passes through your estate. Your spouse already owns the other half.

This can be beneficial (it simplifies transfers between spouses) or problematic (if your estate plan doesn't account for community property rules, assets may not go where you intended). An estate planning attorney who understands California community property law — and how it interacts with trust structures, beneficiary designations, and asset protection — is essential.

The Federal Estate Tax (And Why It's Probably Not Your Problem)

Under the One Big Beautiful Bill Act (signed July 2025), the federal estate tax exemption is $15 million per individual and $30 million per married couple. This exemption is now permanent and will be indexed for inflation starting in 2027. California does not impose a separate state estate tax.

For a 34-year-old physician with a current estate of $500,000 to $1 million, the federal estate tax is extremely unlikely to be an issue in your lifetime. Your estate plan should be designed primarily around probate avoidance, incapacity planning, guardian designation, and asset protection — not tax minimization.

That said, physician incomes compound. A 34-year-old earning $340,000 who saves aggressively, benefits from career growth, and builds equity in a Southern California home could realistically have a $5 to $10 million estate by their 60s. Estate tax planning may become relevant later — but the foundation you build now (the trust structure, the ownership titling, the beneficiary architecture) is what makes future planning possible. The best time to build the framework is before you need it.

We explored how physicians can use these structures to build multi-generational wealth in our post on estate planning essentials for building generational wealth as a physician.

The 20-Minute Checklist

Before you call an attorney, take 20 minutes to gather the information that will make your first meeting productive:

1. List your assets and approximate values: home, retirement accounts (401k, 403b, IRA), brokerage accounts, life insurance policies, bank accounts, vehicles, any business interests.

2. List your debts: mortgage, student loans, car loans, credit cards.

3. Identify beneficiaries on every account: pull up your 401(k), IRA, and life insurance policy and write down who's currently named. These override your will and trust — if they're wrong, fix them.

4. Decide on guardians: if both parents die, who raises your children? Name a first choice and a backup. This is the hardest decision in the entire process. Have the conversation with your spouse before the meeting.

5. Think about successor trustee: who manages the trust if you and your spouse both die or become incapacitated? A family member, a friend, a professional trustee? This person will make financial decisions for your children's inheritance.

6. Gather your insurance policies: malpractice, disability, life, umbrella liability. Your attorney needs to understand the full protection picture.

The Bottom Line

Estate planning at 34 isn't about contemplating your mortality. It's about building the legal infrastructure that protects the people and the wealth you've sacrificed a decade of your life to create.

You spent four years in medical school, three to seven years in residency, maybe more in fellowship — all to build the career and the income that supports your family. A trust-based estate plan, properly structured and funded, ensures that everything you've built transfers smoothly, privately, and on your terms — whether you die, become incapacitated, or simply continue building wealth for the next 30 years.

The cost of getting it done is $2,500 to $5,000. The cost of not getting it done — in probate fees, court delays, lost asset protection, and a judge deciding who raises your children — is incalculable.

Sources Cited

- California Probate Code §10810: Statutory probate fee schedule (4% of first $100K, 3% of next $100K, 2% of next $800K, 1% of next $9M). Fees apply to both attorney and personal representative.

- California Courts Self-Help Guide, "Overview of Formal Probate" (2026): 9–18 month typical timeline, $435 court filing fee. courts.ca.gov

- Opelon LLP, "California Probate Guide 2026": $46,000 combined statutory fees on $1M estate; 12–18 months typical duration; trust-based assets transfer in 30–90 days. opelon.com

- California Probate Code §13100: Small estate affidavit threshold $208,850 (effective April 1, 2025).

- One Big Beautiful Bill Act (P.L. 119-21, signed July 4, 2025): Federal estate tax exemption $15M/individual, $30M/couple, permanent, indexed for inflation starting 2027.

- Social Security Administration: 1 in 4 of today's 20-year-olds will experience a disability before retirement.

- Law Offices of Rozsa Gyene, "How Much Does Probate Cost in California" and "California Probate Timeline" (2026). livingtrust-attorneys.com

- Medscape, Physician Compensation Report 2026. medscape.com

- California Family Code §760: Community property presumption for assets acquired during marriage.

This article is for informational and educational purposes only and should not be considered legal, tax, or financial advice. Estate planning laws vary by state and individual circumstances. The information provided reflects California law as of mid-2026 and may change. Consult with a qualified estate planning attorney licensed in your state before making estate planning decisions.